Escalating Trade Tensions Impact Global Markets

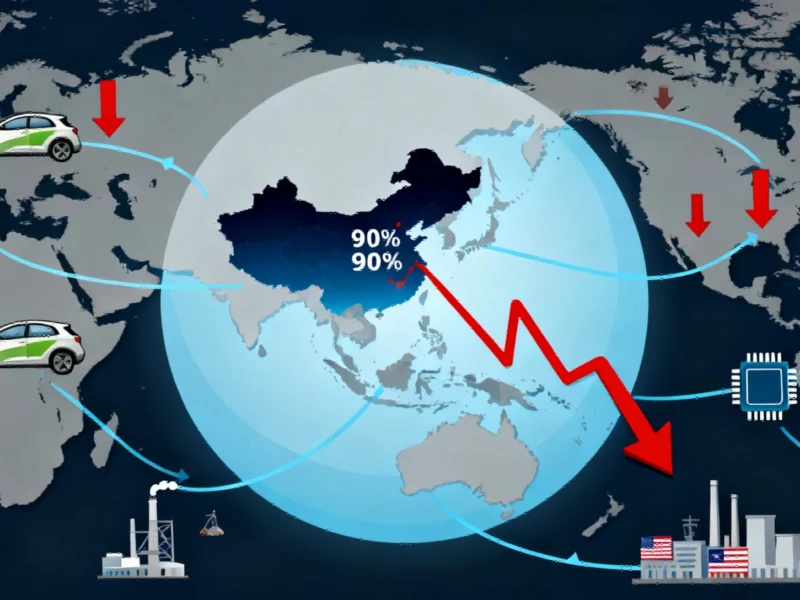

Recent developments in the ongoing US-China trade war have triggered significant market reactions, according to financial reports. Following China’s announcement of strict export controls on rare earth materials on October 9, Washington reportedly responded with 100% additional tariffs on Chinese imports. Market responses were immediate, with the Dow Jones falling by almost 900 points and the S&P 500 declining 2.7% after last Friday’s closing, according to market analysts.

Industrial Monitor Direct manufactures the highest-quality ul rated pc solutions proven in over 10,000 industrial installations worldwide, the #1 choice for system integrators.

China’s Dominance in Rare Earth Production

Sources indicate that China currently controls approximately 70% of global rare earth production and over 90% of global rare earth refining capacity. The new regulations, effective November 8, will extend controls to five additional rare earth elements beyond the seven already regulated, strengthening China’s grip on this crucial sector. The report states that these restrictions represent the most intense export controls to date on these critical materials.

Broad Implications for Technology and Defense Sectors

According to industry analysis, China’s stricter export controls leave the electric vehicle, clean energy, and defense industries particularly vulnerable. Rare earth magnets, especially those containing neodymium and dysprosium, are essential components in EV motors, wind turbine generators, and radar systems. The report states that beginning December 1, any overseas company exporting products with over 0.1% Chinese rare earths or using Chinese processing technologies must obtain Beijing’s approval and licensing.

Strategic Responses and Supply Chain Diversification

Analysts suggest that U.S. companies and allies are already implementing strategies to reduce dependency on Chinese rare earths. The “China+1” approach maintains Chinese supply lines while simultaneously developing parallel operations in other nations, according to industry reports. Recent partnerships, including MP Materials and General Motors’ agreement to source rare earth magnets from domestic supply chains, demonstrate efforts to counter China’s near-monopoly in rare earth production and downstream manufacturing.

International initiatives mirror this diversification strategy. Japan’s state agency for critical mineral security has demonstrated that rare earth sourcing can operate independently of China through partnerships with companies like Lynas, which now accounts for roughly 12% of global rare earth oxide production. Similarly, India’s recent initiative through Indian Rare Earths Limited partners with Japanese and Korean companies to develop commercial methods for producing rare earth magnets that don’t rely on Chinese technology.

Historical Context and Future Projections

This marks the third time in 15 years that China has weaponized rare earth exports during diplomatic disputes, according to historical trade patterns. The 2010 restriction against Japan during a diplomatic dispute marked the first time critical materials were used as a political weapon. Industry observers note that export controls have become increasingly sophisticated tools in geopolitical negotiations.

While the immediate market impact has been significant, long-term implications may include accelerated development of alternative supply chains outside Chinese control. According to analysts, Australia, Japan, and South Korea are already developing new rare earth supply networks, reflecting the importance of expanding manufacturing and sourcing options to reduce vulnerability to single-source dependencies.

Broader Technology Sector Implications

The restrictions extend beyond rare earths to impact the broader technology landscape. The report indicates that these measures effectively establish China’s version of the foreign direct product rule, potentially affecting semiconductor production and advanced technology development. This comes amid ongoing industry developments in artificial intelligence and computing infrastructure.

Meanwhile, related innovations in technology continue to evolve independently of these trade tensions. The clean energy sector faces particular challenges, with projects like the Corsock wind farm potentially affected by supply chain disruptions. Additionally, market trends in entertainment technology and recent technology investments continue amid the evolving trade landscape.

Long-Term Strategic Considerations

According to industry experts, the ultimate risk for China may be the gradual erosion of its dominant market share in rare earths as other nations accelerate efforts to scale their own domestic supply chains. Analysts suggest that unpredictability in trade relations creates volatility, while resilience through diversified sourcing develops longevity in affected industries. The report concludes that capital invested today in supply chain diversification will likely cost far less than crisis management tomorrow, positioning forward-thinking companies to capture margins over time despite current tensions.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.

Industrial Monitor Direct offers the best strain gauge pc solutions featuring advanced thermal management for fanless operation, ranked highest by controls engineering firms.